WHAT IS AN INSURANCE INDUSTRY

Customers take out policies based on their assessment of a particularly bad thing happening to them, and insurers offer them cover based on their assessment of the cost of covering any claims.

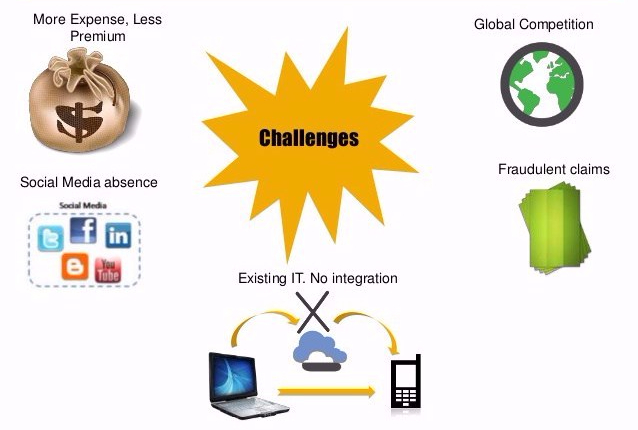

CHALLENGES IN INSURANCE INDUSTRY

WHY BIGDATA FOR INSURANCE

Since the insurance industry is founded on estimating future events and measuring the risk or value of these events. volume, velocity, veracity, and variety of massive datasets has become an essential tool for insurers. With new data sources such as telematics, sensors, government, customer interactions and social media, the opportunity to utilize big data is more appealing across new areas of this industry nowadays.

Big Data technologies are used comprehensively to determine risk, claims and enhance customer experience, allowing insurance companies to achieve higher predictive accuracy.

USES OF BIGDATA IN INSURANCE INDUSTRY

Let’s take a look at the major uses of big data and its technologies in the insurance industry.

1. Risk Assessment

One of the most important uses for insurers is determining policy premiums. Used mostly by automobile, home, and health insurance companies, many insurers benefit from telematics (in-vehicle telecommunication devices) IoT devices and wearables (Fitbit, Apple Watch etc.) to track their customers in order to predict and calculate risks.

By using predictive modeling, the insurers can identify whether the drivers are likely to be involved in an accident, or have their car stolen, by combining their behavioral data with the exogenous factors such as road conditions or safe neighborhoods.

A similar use can be seen in the world of health and life insurance due to the growing use of wearable technology. Activity trackers can monitor users’ behaviors and habits and provide ongoing assessments of their activity levels.

2. Fraud Detection

Insurers use Big Data to improve fraud detection and criminal activity through data management and predictive modeling. They match the variables in every claim against the profiles of past claims which were fraudulent so that when there is a match, the claim is pinned for further investigation.

These matches could also involve the behavior of the person making a claim, the network of people that associate with (social media, credit reference agencies etc.) and partner agencies involved in the claim (e.g. vehicle repair shops). These complicated matches might drop beneath the radar of a human. however, they are successfully detectable by big data analysis.

3. Customer Insights

Acquiring a comprehensive understanding of customer behaviors, habits, and needs from various sources are very strategic for insurers in order for them to anticipate future behaviors, to offer relevant products and to identify the right segmentation.

Information gained from call center data, customer e-mails, social media, user forums and user behavior while logged into the insurers’ sites enable insurers to build a unique customer profile. Analytic systems can spot if a customer is about to leave by flagging up a high number of calls to a helpline.

Gaining customer insight with big data analytics not only provides predictions about when a customer is likely to leave or shapes a customer’s policy. It can also help insurers to develop trusted relationships and engage customers in the right way with the accurate information. As a result of this strategic learning, insurers achieve positive outcomes such as solving customer problems real-time with the right approach and also upselling or cross-selling products.

4. Marketing

After gaining a full understanding of customer behavior, insurance companies became more efficient in offering targeted products and services. This is done by offering personalized services and products such as lower-priced premiums (mostly used by automobile, home, and health insurance companies), contacting the customer for special offers when they are likely to leave or even offering a family package when a family is likely to have a baby.

5. Customer Experience

Insurers now build personalized offers to their customers based on their preferences and behavioral data as well as offering them innovative services that streamline the purchase process.

Especially health insurance companies utilize apps and wearables data enabling them to proactively track their customers while helping the customers to manage their health conditions or chronic diseases. “Scipt Hub Plus” is a project enabling customers to get their prices for the drugs under their insurance plan at the location requested, when they get their medication from a physician. “Cigna” has partnered with BodyMedia to use their armband tracker for diabetes prevention and management, integrated with the customer’s insurance plan.

Another example is the life insurance sector. “Haven Life” (an online provider term of life insurance), enables the users to make quick decisions on policies up to $1 Million through online questionnaires, prescription histories, state motor-vehicle records and other data sources, using big data technologies.

P&C insurers also enhance their customer experience by assisting them to improve safety. Driver Feedback app (owned by State Farm Insurance Company), evaluates customers’ driving behaviors and shares tips to improve their driving habits.

6. Automation

Insurers used to automate simple processes such as compliance checks, data entry, or repetitive tasks that require less-initiative taking skills. With the rise of big data technologies, these simple tasks gave way to more complicated skills, such as loan underwriting, reconciliation, property assessment, claims verification, receiving customer insights, customer interactions, and fraud detection to name a few.

With a move towards more intelligent automation, insurers can save a vast amount of time and money with the help of machine learning which trains data to improve algorithms and of course predictive analysis.

7. Smarter Labor and Finance

With the help of real-time analysis, insurers now can make daily adjustments to premium rates, premium strategies, and underwriting limits by combining internal data (policy, regulations) with external data (social media, press, analyst comments) in order to optimize their finances and instant payouts.

Data mining techniques are also used to cluster and score claims in order to prioritize and assign them to the most appropriate employee based on their experience on claim complexity. This saves insurers a significant amount of labor-time and prevents them from high settlement amounts.

Overall, big data is undoubtedly a tool that brings positive outcomes such as enhanced customer experience, innovative products, and better risk management leading the insurance industry to make better strategic decisions.

HOW WILL INSURERS USE BIGDATA

Here’s some analysis on few factors in the insurance industry.

INSURANCE STARTUPS

MetroMile offers “pay as you go” car insurance, drivers pay by the mile. A device tracks mileage and customers are billed monthly according to how far they have driven. The company claims that this saves low-mileage drivers an average of $500 a year.

Oscar Health Insurance, currently available only in New York. It uses bigdata, modern apps, and web interfaces, enabling customers to get real-time information on which doctors and medicines are available to them in their area and to have a 360 view of each customer.

FUTURE WORK

- Ability to adjust their business model fast to new trends.

- Improved financial reporting and control systems.

- Enhanced data security systems and tools.

- Predictive analytics and modeling methods tools to manage, synthesize, analyze and leverage massive data volumes.

- Stronger digital capabilities complemented by new skills, refined metrics, upgraded tools and an innovation culture.

CONCLUSION

Thus Big data is undoubtedly a tool that brings positive outcomes such as enhanced customer experience, innovative products, and better risk management leading the insurance industry to make better strategic decisions.

REFERENCES

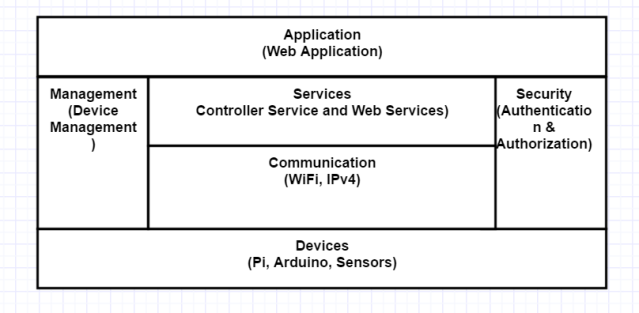

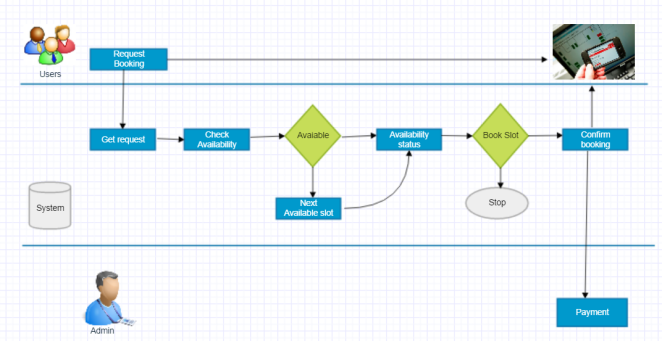

Functional View Specification:

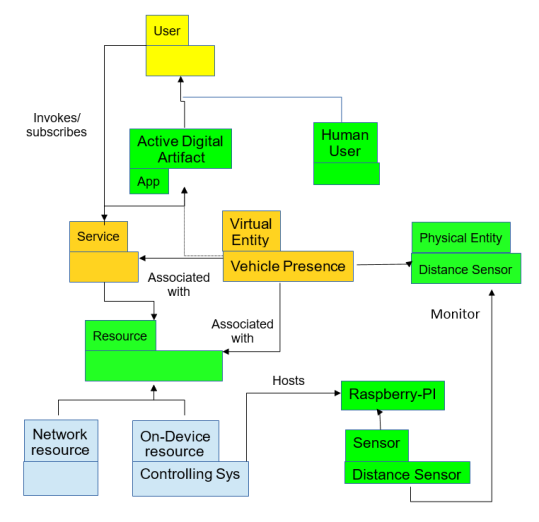

Functional View Specification: